Advanced Examples

- Coefficients/equations

- Exponentiated coefficients (odds ratio, hazard ratio)

- Marginal effects

- Multiple-equation models

- Table of effects signs, significance stars, or "significant signs"

- Add a hypotheses column

- Indicate whether groups of control variables are in the model or not

- Display reference category information

- Adding extra rows using the refcat() option

- Match coefficients across models

- Model summary statistics

- Display summary statistics only (suppress coefficients)

- Adding likelihood-ratio test statistics

- Rearranging the summary statistics in the table footer

- Combining multiple summary statistics in one cell

- Specific models

- Tabulate results from factor

- Clean out table after ologit or oprobit

- Marginal effects for all outcomes after mlogit

- Transforming random-effects parameters of an xtmixed model

- LaTeX

- Descriptive tables

- Table of descriptives

- Table of descriptives by subgroups

- Tabulating results from t-Tests

- Frequency tables

- Other

Coefficients/equations

Exponentiated coefficients (odds ratio, hazard ratio)

To report exponentiated coefficients (aka odds ratio in logistic regression, harzard ratio in the Cox model, incidence rate ratio, relative risk ratio), apply the eform option. Example:

. sysuse auto

(1978 Automobile Data)

. eststo: quietly logit foreign mpg

(est1 stored)

. eststo: quietly logit foreign mpg weight

(est2 stored)

. esttab, eform

--------------------------------------------

(1) (2)

foreign foreign

--------------------------------------------

mpg 1.173** 0.845

(3.04) (-1.83)

weight 0.996***

(-3.86)

--------------------------------------------

N 74 74

--------------------------------------------

Exponentiated coefficients; t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

Note that eform also transforms the standard errors (and confidence intervals), as is illustrated bellow:

. sysuse auto

(1978 Automobile Data)

. quietly logit foreign mpg weight

. eststo raw

. eststo or

. esttab raw or, se mtitles eform(0 1)

--------------------------------------------

(1) (2)

raw or

--------------------------------------------

mpg -0.169 0.845

(0.0919) (0.0777)

weight -0.00391*** 0.996***

(0.00101) (0.00101)

_cons 13.71** 898396.7**

(4.519) (4059591.5)

--------------------------------------------

N 74 74

--------------------------------------------

Standard errors in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

The example also illustrates that, optionally, eform can be applied to selected models only. If you are interested in applying other transformations, see estout's transform() option.

Marginal effects

esttab and estout support Stata's mfx command for calculating marginal effects and elasticities. To make mfx's results available for tabulation it is essential that the model is stored after applying mfx. In esttab or estout then use the margin option to display the marginal effects. Example:

. sysuse auto

(1978 Automobile Data)

. generate reprec = (rep78 > 3) if rep78<.

(5 missing values generated)

. eststo raw: logit foreign mpg reprec

Iteration 0: log likelihood = -42.400729

Iteration 1: log likelihood = -28.036843

Iteration 2: log likelihood = -27.117187

Iteration 3: log likelihood = -27.07727

Iteration 4: log likelihood = -27.07712

Logistic regression Number of obs = 69

LR chi2(2) = 30.65

Prob > chi2 = 0.0000

Log likelihood = -27.07712 Pseudo R2 = 0.3614

------------------------------------------------------------------------------

foreign | Coef. Std. Err. z P>|z| [95% Conf. Interval]

-------------+----------------------------------------------------------------

mpg | .1401865 .0653246 2.15 0.032 .0121527 .2682203

reprec | 2.649856 .7380623 3.59 0.000 1.203281 4.096432

_cons | -5.370321 1.519268 -3.53 0.000 -8.348032 -2.392611

------------------------------------------------------------------------------

. eststo mfx: mfx

Marginal effects after logit

y = Pr(foreign) (predict)

= .21890427

------------------------------------------------------------------------------

variable | dy/dx Std. Err. z P>|z| [ 95% C.I. ] X

---------+--------------------------------------------------------------------

mpg | .0239698 .0121 1.98 0.048 .00026 .04768 21.2899

reprec*| .4813761 .11305 4.26 0.000 .25981 .702943 .42029

------------------------------------------------------------------------------

(*) dy/dx is for discrete change of dummy variable from 0 to 1

. esttab, se margin mtitles

--------------------------------------------

(1) (2)

raw mfx

--------------------------------------------

mpg 0.140* 0.0240*

(0.0653) (0.0121)

reprec (d) 2.650*** 0.481***

(0.738) (0.113)

--------------------------------------------

N 69 69

--------------------------------------------

Marginal effects; Standard errors in parentheses

(d) for discrete change of dummy variable from 0 to 1

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

Multiple-equation models

The default in esttab or estout is to arrange the different equations of multiple-equation models in vertical order, as in:

. sysuse auto

(1978 Automobile Data)

. quietly heckman price weight, select(foreign = weight mpg) twostep

. esttab, wide

-----------------------------------------

(1)

price

-----------------------------------------

price

weight 5.284*** (5.89)

_cons -5925.0*** (-3.50)

-----------------------------------------

foreign

weight -0.00234*** (-4.13)

mpg -0.104* (-2.02)

_cons 8.275** (3.24)

-----------------------------------------

mills

lambda 104.9 (0.12)

-----------------------------------------

N 74

-----------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

However, for models such as mlogit or sureg it is sometimes sensible to arrange the equations horizontally, which can be achieved through the use of the unstack option. Example:

. sysuse auto

(1978 Automobile Data)

. sureg (price foreign weight length) (mpg displ = foreign weight)

Seemingly unrelated regression

----------------------------------------------------------------------

Equation Obs Parms RMSE "R-sq" chi2 P

----------------------------------------------------------------------

price 74 3 1967.769 0.5488 89.74 0.0000

mpg 74 2 3.337283 0.6627 145.39 0.0000

displacement 74 2 39.60002 0.8115 318.62 0.0000

----------------------------------------------------------------------

------------------------------------------------------------------------------

| Coef. Std. Err. z P>|z| [95% Conf. Interval]

-------------+----------------------------------------------------------------

price |

foreign | 3575.26 621.7961 5.75 0.000 2356.562 4793.958

weight | 5.691462 .9205043 6.18 0.000 3.887307 7.495618

length | -88.27114 31.4167 -2.81 0.005 -149.8467 -26.69554

_cons | 4506.212 3588.044 1.26 0.209 -2526.225 11538.65

-------------+----------------------------------------------------------------

mpg |

foreign | -1.650029 1.053958 -1.57 0.117 -3.715748 .4156902

weight | -.0065879 .0006241 -10.56 0.000 -.007811 -.0053647

_cons | 41.6797 2.121197 19.65 0.000 37.52223 45.83717

-------------+----------------------------------------------------------------

displacement |

foreign | -25.6127 12.50621 -2.05 0.041 -50.12441 -1.100984

weight | .0967549 .0074051 13.07 0.000 .0822411 .1112686

_cons | -87.23548 25.17001 -3.47 0.001 -136.5678 -37.90317

------------------------------------------------------------------------------

. esttab, unstack scalars(r2 chi2 p) noobs nomtitle

------------------------------------------------------------

(1)

price mpg displacement

------------------------------------------------------------

foreign 3575.3*** -1.650 -25.61*

(5.75) (-1.57) (-2.05)

weight 5.691*** -0.00659*** 0.0968***

(6.18) (-10.56) (13.07)

length -88.27**

(-2.81)

_cons 4506.2 41.68*** -87.24***

(1.26) (19.65) (-3.47)

------------------------------------------------------------

r2 0.549 0.663 0.812

chi2 89.74 145.4 318.6

p 2.50e-19 2.68e-32 6.50e-70

------------------------------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

Table of effects signs, significance stars, or "significant signs"

Tables containing the signs of the coefficients, "significance stars", or "significant signs" (i.e. the signs of the coefficient where each sing is repeated according to significance level) can be produced as follows:

. sysuse auto

(1978 Automobile Data)

. eststo: regress price mpg foreign

Source | SS df MS Number of obs = 74

-------------+------------------------------ F( 2, 71) = 14.07

Model | 180261702 2 90130850.8 Prob > F = 0.0000

Residual | 454803695 71 6405685.84 R-squared = 0.2838

-------------+------------------------------ Adj R-squared = 0.2637

Total | 635065396 73 8699525.97 Root MSE = 2530.9

------------------------------------------------------------------------------

price | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

mpg | -294.1955 55.69172 -5.28 0.000 -405.2417 -183.1494

foreign | 1767.292 700.158 2.52 0.014 371.2169 3163.368

_cons | 11905.42 1158.634 10.28 0.000 9595.164 14215.67

------------------------------------------------------------------------------

(est1 stored)

. eststo: regress price mpg foreign weight

Source | SS df MS Number of obs = 74

-------------+------------------------------ F( 3, 70) = 23.29

Model | 317252881 3 105750960 Prob > F = 0.0000

Residual | 317812515 70 4540178.78 R-squared = 0.4996

-------------+------------------------------ Adj R-squared = 0.4781

Total | 635065396 73 8699525.97 Root MSE = 2130.8

------------------------------------------------------------------------------

price | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

mpg | 21.8536 74.22114 0.29 0.769 -126.1758 169.883

foreign | 3673.06 683.9783 5.37 0.000 2308.909 5037.212

weight | 3.464706 .630749 5.49 0.000 2.206717 4.722695

_cons | -5853.696 3376.987 -1.73 0.087 -12588.88 881.4934

------------------------------------------------------------------------------

(est2 stored)

. esttab, cells(_sign) nogap

--------------------------------------

(1) (2)

price price

_sign _sign

--------------------------------------

mpg - +

foreign + +

weight +

_cons + -

--------------------------------------

N 74 74

--------------------------------------

. esttab, cells(_star) nogap ///

> starlevels(n.s. 1 * 0.05 ** 0.01)

--------------------------------------

(1) (2)

price price

_star _star

--------------------------------------

mpg ** n.s.

foreign * **

weight **

_cons ** n.s.

--------------------------------------

N 74 74

--------------------------------------

. esttab, cells(_sigsign) nogap ///

> starlevels("+/-" 1 "++/--" 0.05 "+++/---" 0.01)

--------------------------------------

(1) (2)

price price

_sigsign _sigsign

--------------------------------------

mpg --- +

foreign ++ +++

weight +++

_cons +++ -

--------------------------------------

N 74 74

--------------------------------------

. eststo clear

Add a hypotheses column

Use the labcol2() option to add a column indicating the expected directions of effects according to theory:

. sysuse auto

(1978 Automobile Data)

. quietly regress price mpg foreign weight displ

. esttab, labcol2(+ ? + -, title("" Hypothesis))

-----------------------------------------

(1)

Hypothesis price

-----------------------------------------

mpg + 19.08

(0.26)

foreign ? 3930.2***

(5.67)

weight + 2.458**

(2.82)

displacement - 10.22

(1.65)

_cons -4846.8

(-1.43)

-----------------------------------------

N 74

-----------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

Indicate whether groups of control variables are in the model or not

To save space full output is sometimes suppressed for certain control variables and it is only indicated whether the model contains the variables or not. The indicate() in estout supports the construction of such tables:

. sysuse auto

(1978 Automobile Data)

. eststo: quietly regress price mpg foreign

(est1 stored)

. eststo: xi: quietly regress price mpg foreign i.rep78

i.rep78 _Irep78_1-5 (naturally coded; _Irep78_1 omitted)

(est2 stored)

. esttab, indicate(rep dummies = _Irep78*)

--------------------------------------------

(1) (2)

price price

--------------------------------------------

mpg -294.2*** -299.6***

(-5.28) (-4.73)

foreign 1767.3* 1102.3

(2.52) (1.22)

_cons 11905.4*** 10856.2***

(10.28) (4.79)

rep dummies No Yes

--------------------------------------------

N 74 69

--------------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

indicate() prints its information at the bottom of the main body of the table containing the coefficients. If you want to include the information in the table footer, then use the following approach:

. sysuse auto

(1978 Automobile Data)

. eststo: quietly regress price mpg foreign

(est1 stored)

. estadd local hasrep "No"

added macro:

e(hasrep) : "No"

. eststo: xi: quietly regress price mpg foreign i.rep78

i.rep78 _Irep78_1-5 (naturally coded; _Irep78_1 omitted)

(est2 stored)

. estadd local hasrep "Yes"

added macro:

e(hasrep) : "Yes"

. esttab, drop(_Irep78*) scalars("hasrep rep dummies")

--------------------------------------------

(1) (2)

price price

--------------------------------------------

mpg -294.2*** -299.6***

(-5.28) (-4.73)

foreign 1767.3* 1102.3

(2.52) (1.22)

_cons 11905.4*** 10856.2***

(10.28) (4.79)

--------------------------------------------

N 74 69

rep dummies No Yes

--------------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

Display reference category information

Use the refcat() option to add a table row containing the (omitted) reference category of a categorical variable. Example:

. sysuse cancer

(Patient Survival in Drug Trial)

. stset studytime, failure(died)

failure event: died != 0 & died < .

obs. time interval: (0, studytime]

exit on or before: failure

------------------------------------------------------------------------------

48 total obs.

0 exclusions

------------------------------------------------------------------------------

48 obs. remaining, representing

31 failures in single record/single failure data

744 total analysis time at risk, at risk from t = 0

earliest observed entry t = 0

last observed exit t = 39

. xi: stcox age i.drug, nolog

i.drug _Idrug_1-3 (naturally coded; _Idrug_1 omitted)

failure _d: died

analysis time _t: studytime

Cox regression -- Breslow method for ties

No. of subjects = 48 Number of obs = 48

No. of failures = 31

Time at risk = 744

LR chi2(3) = 36.52

Log likelihood = -81.652567 Prob > chi2 = 0.0000

------------------------------------------------------------------------------

_t | Haz. Ratio Std. Err. z P>|z| [95% Conf. Interval]

-------------+----------------------------------------------------------------

age | 1.118334 .0409074 3.06 0.002 1.040963 1.201455

_Idrug_2 | .1805839 .0892742 -3.46 0.001 .0685292 .4758636

_Idrug_3 | .0520066 .034103 -4.51 0.000 .0143843 .1880305

------------------------------------------------------------------------------

. lab var _Idrug_2 "Tadalafil"

. lab var _Idrug_3 "Sildenafil"

. esttab, eform wide label nostar refcat(_Idrug_2 "Placebo")

----------------------------------------------

(1)

_t

----------------------------------------------

Patient's age at s.. 1.118 (3.06)

Placebo ref.

Tadalafil 0.181 (-3.46)

Sildenafil 0.0520 (-4.51)

----------------------------------------------

Observations 48

----------------------------------------------

Exponentiated coefficients; t statistics in parentheses

. esttab, eform wide label nostar refcat(_Idrug_2 "Placebo", label(1))

----------------------------------------------

(1)

_t

----------------------------------------------

Patient's age at s.. 1.118 (3.06)

Placebo 1

Tadalafil 0.181 (-3.46)

Sildenafil 0.0520 (-4.51)

----------------------------------------------

Observations 48

----------------------------------------------

Exponentiated coefficients; t statistics in parentheses

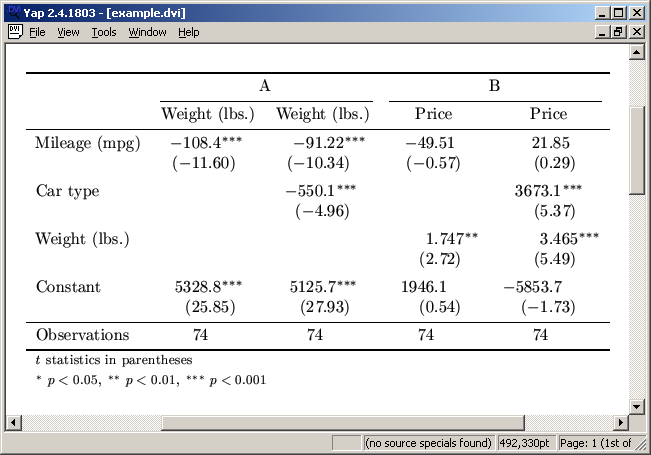

Adding extra rows using the refcat() option

The refcat() option is designed to include information on the (omitted) reference category of a categorical variable (see above), but it can also be used to include extra rows in the table containing subtitles or other information. Example:

. sysuse auto

(1978 Automobile Data)

. regress price weight mpg turn foreign

Source | SS df MS Number of obs = 74

-------------+------------------------------ F( 4, 69) = 19.23

Model | 334771309 4 83692827.3 Prob > F = 0.0000

Residual | 300294087 69 4352088.22 R-squared = 0.5271

-------------+------------------------------ Adj R-squared = 0.4997

Total | 635065396 73 8699525.97 Root MSE = 2086.2

------------------------------------------------------------------------------

price | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

weight | 4.284532 .7404967 5.79 0.000 2.807282 5.761783

mpg | -.4660076 73.51407 -0.01 0.995 -147.1226 146.1905

turn | -229.2059 114.2423 -2.01 0.049 -457.1131 -1.298676

foreign | 3221.415 706.4847 4.56 0.000 1812.017 4630.813

_cons | 1368.197 4887.597 0.28 0.780 -8382.292 11118.69

------------------------------------------------------------------------------

. foreach v of varlist weight mpg turn foreign {

2. label variable `v' `"- `: variable label `v''"'

3. }

. esttab, refcat(weight "Main effects:" turn "Controls:", nolabel) wide label

-------------------------------------------------

(1)

Price

-------------------------------------------------

Main effects:

- Weight (lbs.) 4.285*** (5.79)

- Mileage (mpg) -0.466 (-0.01)

Controls:

- Turn Circle (ft.) -229.2* (-2.01)

- Car type 3221.4*** (4.56)

Constant 1368.2 (0.28)

-------------------------------------------------

Observations 74

-------------------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

Match coefficients across models

Rename coefficients using the rename() option before matching the models and equations to merge different coefficients into the same table row. Example:

. sysuse auto

(1978 Automobile Data)

. set seed 123

. generate altmpg = invnorm(uniform())

. eststo: quietly regress price weight mpg

(est1 stored)

. eststo: quietly regress price weight altmpg

(est2 stored)

. esttab

--------------------------------------------

(1) (2)

price price

--------------------------------------------

weight 1.747** 2.037***

(2.72) (5.36)

mpg -49.51

(-0.57)

altmpg -73.94

(-0.29)

_cons 1946.1 6.433

(0.54) (0.01)

--------------------------------------------

N 74 74

--------------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. esttab, rename(altmpg mpg)

--------------------------------------------

(1) (2)

price price

--------------------------------------------

weight 1.747** 2.037***

(2.72) (5.36)

mpg -49.51 -73.94

(-0.57) (-0.29)

_cons 1946.1 6.433

(0.54) (0.01)

--------------------------------------------

N 74 74

--------------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

Model summary statistics

Display summary statistics only (suppress coefficients)

If you want to produce a table that only contains the summary statistics of the models, but no coefficients, add cells(none) to the command:

. sysuse auto

(1978 Automobile Data)

. eststo: quietly regress price weight mpg

(est1 stored)

. eststo: quietly regress price weight mpg foreign

(est2 stored)

. esttab, cells(none) scalars(rank r2 r2_a bic aic) nomtitles

--------------------------------------

(1) (2)

--------------------------------------

N 74 74

rank 3 4

r2 0.293 0.500

r2_a 0.273 0.478

bic 1378.6 1357.4

aic 1371.7 1348.2

--------------------------------------

. eststo clear

Adding likelihood-ratio test statistics

The estadd's lrtest subcommand may be used to add results from likelihood-ratio tests as follows:

. sysuse auto

(1978 Automobile Data)

. eststo A: quietly logit foreign weight

. eststo B: quietly logit foreign weight mpg price

. estadd lrtest A

Likelihood-ratio test LR chi2(2) = 23.78

(Assumption: A nested in .) Prob > chi2 = 0.0000

added scalars:

e(lrtest_p) = 6.844e-06

e(lrtest_chi2) = 23.784217

e(lrtest_df) = 2

. esttab, scalars(lrtest_chi2 lrtest_df lrtest_p)

--------------------------------------------

(1) (2)

foreign foreign

--------------------------------------------

weight -0.00259*** -0.00685***

(-4.25) (-3.43)

mpg -0.121

(-1.27)

price 0.000926**

(3.01)

_cons 6.283*** 14.42**

(3.92) (2.66)

--------------------------------------------

N 74 74

lrtest_chi2 23.78

lrtest_df 2

lrtest_p 0.00000684

--------------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

Rearranging the summary statistics in the table footer

The default in estout and esttab is to print the scalar summary statistics in the table footer in separate rows beneath one another (in each model's first column). Use the layout() suboption in the stats() option to rearrange the statistics. The option allows you to place the statistics in separate columns beside one another or also to combine multiple statistics in one table cell (see below). Here is an example:

. sysuse auto

(1978 Automobile Data)

. eststo: quietly regress price weight

(est1 stored)

. eststo: quietly regress price weight foreign

(est2 stored)

. esttab, p wide nopar label ///

> stats(F p N, layout("@ @" @) fmt(a3 3 a3) ///

> labels("F statistic" "Observations"))

------------------------------------------------------------------------------

(1) (2)

Price Price

------------------------------------------------------------------------------

Weight (lbs.) 2.044*** 0.000 3.321*** 0.000

Car type 3637.0*** 0.000

Constant -6.707 0.995 -4942.8*** 0.000

------------------------------------------------------------------------------

F statistic 29.42 0.000 35.35 0.000

Observations 74 74

------------------------------------------------------------------------------

p-values in second column

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

In the layout() suboption, the "@" character is used as a placeholder for the statistics, one after another. Statistics to be printed in the same row have to be enclosed in quotes.

Combining multiple summary statistics in one cell

The syntax for combining multiple summary statistics in one table cell is a bit clumsy, as is illustrated in the following example. The cell definition has to be enclosed in double quotes in the example because it contains a blank, and a set of compound double quotes is needed to mark off the row definition.

. sysuse auto

(1978 Automobile Data)

. eststo: quietly logit foreign weight mpg

(est1 stored)

. eststo: quietly logit foreign weight mpg turn displ

(est2 stored)

. esttab, stats(chi2 df_m r2_p N, layout(`""@ (@)""' @ @))

--------------------------------------------

(1) (2)

foreign foreign

--------------------------------------------

weight -0.00391*** 0.00239

(-3.86) (0.99)

mpg -0.169 -0.196*

(-1.83) (-2.07)

turn -0.502*

(-2.28)

displacement -0.0769*

(-2.06)

_cons 13.71** 26.95**

(3.03) (3.00)

--------------------------------------------

chi2 (df_m) 35.72 (2) 55.82 (4)

r2_p 0.397 0.620

N 74 74

--------------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

Note that in this example the layout definition could be simplified to layout(`""@ (@)""') without changing the result.

Specific models

Tabulate results from factor

The factor command does not return e(b) and e(V), which makes tabulation less obvious. For example, the factor loadings are returned in matrix e(L) and the unique variances are returned in e(Psi):

. webuse bg2

(Physician-cost data)

. factor bg2cost1-bg2cost6

(obs=568)

Factor analysis/correlation Number of obs = 568

Method: principal factors Retained factors = 3

Rotation: (unrotated) Number of params = 15

--------------------------------------------------------------------------

Factor | Eigenvalue Difference Proportion Cumulative

-------------+------------------------------------------------------------

Factor1 | 0.85389 0.31282 1.0310 1.0310

Factor2 | 0.54107 0.51786 0.6533 1.6844

Factor3 | 0.02321 0.17288 0.0280 1.7124

Factor4 | -0.14967 0.03951 -0.1807 1.5317

Factor5 | -0.18918 0.06197 -0.2284 1.3033

Factor6 | -0.25115 . -0.3033 1.0000

--------------------------------------------------------------------------

LR test: independent vs. saturated: chi2(15) = 269.07 Prob>chi2 = 0.0000

Factor loadings (pattern matrix) and unique variances

-----------------------------------------------------------

Variable | Factor1 Factor2 Factor3 | Uniqueness

-------------+------------------------------+--------------

bg2cost1 | 0.2470 0.3670 -0.0446 | 0.8023

bg2cost2 | -0.3374 0.3321 -0.0772 | 0.7699

bg2cost3 | -0.3764 0.3756 0.0204 | 0.7169

bg2cost4 | -0.3221 0.1942 0.1034 | 0.8479

bg2cost5 | 0.4550 0.2479 0.0641 | 0.7274

bg2cost6 | 0.4760 0.2364 -0.0068 | 0.7175

-----------------------------------------------------------

. ereturn list

scalars:

e(f) = 3

e(N) = 568

e(df_m) = 15

e(df_r) = 0

e(chi2_i) = 269.0736870812582

e(df_i) = 15

e(p_i) = 1.43900835150e-48

e(evsum) = .8281790835746108

macros:

e(cmdline) : "factor bg2cost1-bg2cost6"

e(cmd) : "factor"

e(properties) : "nob noV eigen"

e(title) : "Factor analysis"

e(predict) : "factor_p"

e(estat_cmd) : "factor_estat"

e(rotate_cmd) : "factor_rotate"

e(mtitle) : "principal factors"

e(method) : "pf"

matrices:

e(sds) : 1 x 6

e(means) : 1 x 6

e(C) : 6 x 6

e(Phi) : 3 x 3

e(L) : 6 x 3

e(Psi) : 1 x 6

e(Ev) : 1 x 6

functions:

e(sample)

. matrix list e(L)

e(L)[6,3]

Factor1 Factor2 Factor3

bg2cost1 .24704957 .36703122 -.04457883

bg2cost2 -.33741222 .33210838 -.07721559

bg2cost3 -.37640773 .3755668 .02035389

bg2cost4 -.32206954 .1941843 .10341942

bg2cost5 .45501598 .24785063 .06407803

bg2cost6 .47598434 .23638092 -.0067801

. matrix list e(Psi)

e(Psi)[1,6]

bg2cost1 bg2cost2 bg2cost3 bg2cost4 bg2cost5 bg2cost6

Uniqueness .80226732 .76989477 .71685252 .84786809 .72742453 .717517

The simplest way to tabulate the factor loadings is to type:

. esttab e(L)

---------------------------------------------------

e(L)

Factor1 Factor2 Factor3

---------------------------------------------------

bg2cost1 .2470496 .3670312 -.0445788

bg2cost2 -.3374122 .3321084 -.0772156

bg2cost3 -.3764077 .3755668 .0203539

bg2cost4 -.3220695 .1941843 .1034194

bg2cost5 .455016 .2478506 .064078

bg2cost6 .4759843 .2363809 -.0067801

---------------------------------------------------

Reproducing the factor loadings table including the unique variances is more involved. The single factors in e(L) have to be addressed individually. For example, type:

. esttab, ///

> cells("L[1](transpose) L[2](transpose) L[3](transpose) Psi") ///

> nogap noobs nonumber nomtitle

----------------------------------------------------------------

L[1] L[2] L[3] Psi

----------------------------------------------------------------

bg2cost1 .2470496 .3670312 -.0445788 .8022673

bg2cost2 -.3374122 .3321084 -.0772156 .7698948

bg2cost3 -.3764077 .3755668 .0203539 .7168525

bg2cost4 -.3220695 .1941843 .1034194 .8478681

bg2cost5 .455016 .2478506 .064078 .7274245

bg2cost6 .4759843 .2363809 -.0067801 .717517

----------------------------------------------------------------

The transpose suboption is required since the factors are in the columns of e(L) and, by default, e()-matrices are read row-wise (transpose can be abbreviated to t). Hence, L[#](transpose) refers to the #th column of e(L).

The label() suboption can be used to add labels, for example:

. esttab, ///

> cells("L[1](t label(Factor 1)) L[2](t) L[3](t) Psi") ///

> nogap noobs nonumber nomtitle

----------------------------------------------------------------

Factor 1 L[2] L[3] Psi

----------------------------------------------------------------

bg2cost1 .2470496 .3670312 -.0445788 .8022673

bg2cost2 -.3374122 .3321084 -.0772156 .7698948

bg2cost3 -.3764077 .3755668 .0203539 .7168525

bg2cost4 -.3220695 .1941843 .1034194 .8478681

bg2cost5 .455016 .2478506 .064078 .7274245

bg2cost6 .4759843 .2363809 -.0067801 .717517

----------------------------------------------------------------

Alternatively, you can also use syntax el[name], where name refers to the name of the row to be tabulated (or column if transpose is specified) and also sets the label:

. esttab, ///

> cells("L[Factor1](t) L[Factor2](t) L[Factor3](t) Psi[Uniqueness]") ///

> nogap noobs nonumber nomtitle

----------------------------------------------------------------

Factor1 Factor2 Factor3 Uniqueness

----------------------------------------------------------------

bg2cost1 .2470496 .3670312 -.0445788 .8022673

bg2cost2 -.3374122 .3321084 -.0772156 .7698948

bg2cost3 -.3764077 .3755668 .0203539 .7168525

bg2cost4 -.3220695 .1941843 .1034194 .8478681

bg2cost5 .455016 .2478506 .064078 .7274245

bg2cost6 .4759843 .2363809 -.0067801 .717517

----------------------------------------------------------------

Clean out table after ologit or oprobit

Tables of ologit or oprobit look somewhat complicated in Stata 9 or newer since each cutoff is stored in its own equation. To clean out the table, specify eqlabels(none):

. sysuse auto

(1978 Automobile Data)

. ologit rep mpg foreign

Iteration 0: log likelihood = -93.692061

Iteration 1: log likelihood = -78.844995

Iteration 2: log likelihood = -78.106784

Iteration 3: log likelihood = -78.08927

Iteration 4: log likelihood = -78.089242

Ordered logistic regression Number of obs = 69

LR chi2(2) = 31.21

Prob > chi2 = 0.0000

Log likelihood = -78.089242 Pseudo R2 = 0.1665

------------------------------------------------------------------------------

rep78 | Coef. Std. Err. z P>|z| [95% Conf. Interval]

-------------+----------------------------------------------------------------

mpg | .0672774 .0494465 1.36 0.174 -.029636 .1641908

foreign | 2.599085 .6745627 3.85 0.000 1.276966 3.921204

-------------+----------------------------------------------------------------

/cut1 | -1.885212 1.175719 -4.189579 .4191555

/cut2 | -.0922328 .9934139 -2.039288 1.854823

/cut3 | 2.524538 1.021289 .5228488 4.526228

/cut4 | 4.580877 1.146847 2.333098 6.828657

------------------------------------------------------------------------------

. esttab, wide

-----------------------------------------

(1)

rep78

-----------------------------------------

rep78

mpg 0.0673 (1.36)

foreign 2.599*** (3.85)

-----------------------------------------

cut1

_cons -1.885 (-1.60)

-----------------------------------------

cut2

_cons -0.0922 (-0.09)

-----------------------------------------

cut3

_cons 2.525* (2.47)

-----------------------------------------

cut4

_cons 4.581*** (3.99)

-----------------------------------------

N 69

-----------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. esttab, wide eqlabels(none)

-----------------------------------------

(1)

rep78

-----------------------------------------

mpg 0.0673 (1.36)

foreign 2.599*** (3.85)

cut1 -1.885 (-1.60)

cut2 -0.0922 (-0.09)

cut3 2.525* (2.47)

cut4 4.581*** (3.99)

-----------------------------------------

N 69

-----------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

To print a line between the main part of the table and the cutoffs, type:

. esttab, wide eqlabels(none) ///

> varlabels(,blist(cut1:_cons "{hline @width}{break}"))

-----------------------------------------

(1)

rep78

-----------------------------------------

mpg 0.0673 (1.36)

foreign 2.599*** (3.85)

-----------------------------------------

cut1 -1.885 (-1.60)

cut2 -0.0922 (-0.09)

cut3 2.525* (2.47)

cut4 4.581*** (3.99)

-----------------------------------------

N 69

-----------------------------------------

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

Furthermore, to suppress significance stars and standard errors for the cutoffs, type:

. esttab, cells("b(fmt(a3) star) se(drop(cut*:))") ///

> stardrop(cut*:) eqlabels(none) ///

> varlabels(,blist(cut1:_cons "{hline @width}{break}"))

-----------------------------------------

(1)

rep78

b se

-----------------------------------------

mpg 0.0673 0.0494

foreign 2.599*** 0.675

-----------------------------------------

cut1 -1.885

cut2 -0.0922

cut3 2.525

cut4 4.581

-----------------------------------------

N 69

-----------------------------------------

Marginal effects for all outcomes after mlogit

To tabulate the marginal effects for all outcomes after mlogit it is necessary to store several variants of the model's estimates. Example:

. sysuse auto

(1978 Automobile Data)

. replace price = price / 1000

price was int now float

(74 real changes made)

. replace weight = weight / 1000

weight was int now float

(74 real changes made)

. quietly mlogit rep78 price mpg foreign if rep78>=3, nolog

. foreach o in 3 4 5 {

2. eststo, title(Outcome `o'): quietly mfx, predict(outcome(`o')) nose

3. }

(est1 stored)

(est2 stored)

(est3 stored)

. esttab, margin scalars(Xmfx_y) noobs not nostar nocons ///

> mtitles nonumbers keep(4:) eqlabels(none) collabels(none)

---------------------------------------------------

Outcome 3 Outcome 4 Outcome 5

---------------------------------------------------

price -0.00347 -0.0140 0.0175

mpg -0.0171 -0.00245 0.0195

foreign (d) -0.516 0.290 0.225

---------------------------------------------------

Xmfx_y 0.510 0.380 0.110

---------------------------------------------------

Marginal effects

(d) for discrete change of dummy variable from 0 to 1

. eststo clear

Things get involved if the marginal effects for the outcomes be printed beneath one another, because the model's representation in the e()-returns lacks an equation for the reference outcome. However, you can use estadd prchange with the adapt option to compute marginal effects and set up the model for tabulation. Example:

. sysuse auto

(1978 Automobile Data)

. replace price = price / 1000

price was int now float

(74 real changes made)

. replace weight = weight / 1000

weight was int now float

(74 real changes made)

. quietly mlogit rep78 price mpg foreign if rep78>=3, nolog

. estadd prchange, c(margefct) adapt

mlogit: Changes in Probabilities for rep78

price

Avg|Chg| 4 5 3

Min->Max .22632305 -.20621726 .33948457 -.13326731

-+1/2 .01165351 -.01400626 .01748028 -.003474

-+sd/2 .03369502 -.04037875 .05054252 -.01016378

MargEfct .01164741 -.01400459 .01747111 -.00346652

mpg

Avg|Chg| 4 5 3

Min->Max .55527355 -.27560695 .8329103 -.55730341

-+1/2 .01301373 -.0024623 .01952058 -.01705831

-+sd/2 .08165233 -.01687825 .12247847 -.10560027

MargEfct .0130051 -.00245415 .01950765 -.01705351

foreign

Avg|Chg| 4 5 3

0->1 .34368436 .29041834 .22510819 -.51552653

4 5 3

Pr(y|x) .38015294 .11008285 .50976419

price mpg foreign

x= 6.22385 21.5932 .355932

sd(x)= 2.88045 6.13109 .482905

added scalars:

e(predval4) = .38015294

e(predval5) = .11008285

e(predval3) = .50976419

e(delta) = 1

e(centered) = 1

added matrices:

e(dc) : 6 x 9 (main, Min->Max, 0->1, -+1/2, -+sd/2, Marg

> Efct)

e(pattern) : 1 x 9

e(X) : 4 x 3 (X, SD, Min, Max)

first row in e(dc) contains:

01 change for binary variables

margefct for continuous variables

Note: e(b) and e(V) modified - use for tabulation only

. esttab, main(dc) not nostar

-------------------------

(1)

rep78

-------------------------

3

price -0.00347

mpg -0.0171

foreign -0.516

-------------------------

4

price -0.0140

mpg -0.00245

foreign 0.290

-------------------------

5

price 0.0175

mpg 0.0195

foreign 0.225

-------------------------

N 59

-------------------------

dc coefficients

Transforming random-effects parameters of an xtmixed model

Variance parameters are returned by xtmixed as logarithms of standard deviations in e(b). To tabulate the parameters as standard deviations, back-transform them using the transform() option. Example:

. webuse pig

(Longitudinal analysis of pig weights)

. xtmixed weight week || id: week

Performing EM optimization:

Performing gradient-based optimization:

Iteration 0: log restricted-likelihood = -870.51473

Iteration 1: log restricted-likelihood = -870.51473

Computing standard errors:

Mixed-effects REML regression Number of obs = 432

Group variable: id Number of groups = 48

Obs per group: min = 9

avg = 9.0

max = 9

Wald chi2(1) = 4592.10

Log restricted-likelihood = -870.51473 Prob > chi2 = 0.0000

------------------------------------------------------------------------------

weight | Coef. Std. Err. z P>|z| [95% Conf. Interval]

-------------+----------------------------------------------------------------

week | 6.209896 .0916386 67.77 0.000 6.030287 6.389504

_cons | 19.35561 .4021142 48.13 0.000 18.56748 20.14374

------------------------------------------------------------------------------

------------------------------------------------------------------------------

Random-effects Parameters | Estimate Std. Err. [95% Conf. Interval]

-----------------------------+------------------------------------------------

id: Independent |

sd(week) | .6135471 .0673971 .4947035 .7609409

sd(_cons) | 2.630132 .302883 2.098719 3.296105

-----------------------------+------------------------------------------------

sd(Residual) | 1.26443 .0487971 1.172317 1.363781

------------------------------------------------------------------------------

LR test vs. linear regression: chi2(2) = 765.92 Prob > chi2 = 0.0000

Note: LR test is conservative and provided only for reference.

. esttab, se wide nostar transform(ln*: exp(@) exp(@))

--------------------------------------

(1)

weight

--------------------------------------

weight

week 6.210 (0.0916)

_cons 19.36 (0.402)

--------------------------------------

lns1_1_1

_cons 0.614 (0.0674)

--------------------------------------

lns1_1_2

_cons 2.630 (0.303)

--------------------------------------

lnsig_e

_cons 1.264 (0.0488)

--------------------------------------

N 432

--------------------------------------

Standard errors in parentheses

. esttab, se wide nostar transform(ln*: exp(@) exp(@)) ///

> eqlabels("" "sd(week)" "sd(_cons)" "sd(Residual)", none) ///

> varlabels(,elist(weight:_cons "{break}{hline @width}")) ///

> varwidth(13)

---------------------------------------

(1)

weight

---------------------------------------

week 6.210 (0.0916)

_cons 19.36 (0.402)

---------------------------------------

sd(week) 0.614 (0.0674)

sd(_cons) 2.630 (0.303)

sd(Residual) 1.264 (0.0488)

---------------------------------------

N 432

---------------------------------------

Standard errors in parentheses

(Note that in transform() you also have to include the function's first derivative, which is required for the standard errors. The example above might be confusing because the first derivative of exp(x) is simply exp(x). See below for examples where the two differ.)

Similarly, to display the parameters as variances, type:

. xtmixed, variance

Mixed-effects REML regression Number of obs = 432

Group variable: id Number of groups = 48

Obs per group: min = 9

avg = 9.0

max = 9

Wald chi2(1) = 4592.10

Log restricted-likelihood = -870.51473 Prob > chi2 = 0.0000

------------------------------------------------------------------------------

weight | Coef. Std. Err. z P>|z| [95% Conf. Interval]

-------------+----------------------------------------------------------------

week | 6.209896 .0916386 67.77 0.000 6.030287 6.389504

_cons | 19.35561 .4021142 48.13 0.000 18.56748 20.14374

------------------------------------------------------------------------------

------------------------------------------------------------------------------

Random-effects Parameters | Estimate Std. Err. [95% Conf. Interval]

-----------------------------+------------------------------------------------

id: Independent |

var(week) | .3764401 .0827025 .2447315 .579031

var(_cons) | 6.917597 1.593245 4.40462 10.86431

-----------------------------+------------------------------------------------

var(Residual) | 1.598784 .1234011 1.374328 1.859899

------------------------------------------------------------------------------

LR test vs. linear regression: chi2(2) = 765.92 Prob > chi2 = 0.0000

Note: LR test is conservative and provided only for reference.

. esttab, se wide nostar transform(ln*: exp(2*@) 2*exp(2*@)) ///

> eqlabels("" "var(week)" "var(_cons)" "var(Residual)", none) ///

> varlabels(,elist(weight:_cons "{break}{hline @width}")) ///

> varwidth(13)

---------------------------------------

(1)

weight

---------------------------------------

week 6.210 (0.0916)

_cons 19.36 (0.402)

---------------------------------------

var(week) 0.376 (0.0827)

var(_cons) 6.918 (1.593)

var(Residual) 1.599 (0.123)

---------------------------------------

N 432

---------------------------------------

Standard errors in parentheses

If the model also has covariance terms, these are returned as arc-hyperbolic tangents of correlations in e(b) and can be back-transformed to correlations using Stata's tanh() function. Example:

. xtmixed weight week || id: week, covariance(unstructured)

Performing EM optimization:

Performing gradient-based optimization:

Iteration 0: log restricted-likelihood = -870.43562

Iteration 1: log restricted-likelihood = -870.43562

Computing standard errors:

Mixed-effects REML regression Number of obs = 432

Group variable: id Number of groups = 48

Obs per group: min = 9

avg = 9.0

max = 9

Wald chi2(1) = 4552.31

Log restricted-likelihood = -870.43562 Prob > chi2 = 0.0000

------------------------------------------------------------------------------

weight | Coef. Std. Err. z P>|z| [95% Conf. Interval]

-------------+----------------------------------------------------------------

week | 6.209896 .0920382 67.47 0.000 6.029504 6.390287

_cons | 19.35561 .4038677 47.93 0.000 18.56405 20.14718

------------------------------------------------------------------------------

------------------------------------------------------------------------------

Random-effects Parameters | Estimate Std. Err. [95% Conf. Interval]

-----------------------------+------------------------------------------------

id: Unstructured |

sd(week) | .6164379 .0680541 .4964981 .7653519

sd(_cons) | 2.643192 .3057584 2.106996 3.315842

corr(week,_cons) | -.0634377 .158876 -.3593789 .2440973

-----------------------------+------------------------------------------------

sd(Residual) | 1.263657 .0487466 1.171638 1.362903

------------------------------------------------------------------------------

LR test vs. linear regression: chi2(3) = 766.07 Prob > chi2 = 0.0000

Note: LR test is conservative and provided only for reference.

. esttab, se wide nostar ///

> transform(ln*: exp(@) exp(@) at*: tanh(@) (1-tanh(@)^2)) ///

> eqlabels("" "sd(week)" "sd(_cons)" "corr(week,_cons)" "sd(Residual)", ///

> none) ///

> varlabels(,elist(weight:_cons "{break}{hline @width}")) ///

> varwidth(16)

------------------------------------------

(1)

weight

------------------------------------------

week 6.210 (0.0920)

_cons 19.36 (0.404)

------------------------------------------

sd(week) 0.616 (0.0681)

sd(_cons) 2.643 (0.306)

corr(week,_cons) -0.0634 (0.159)

sd(Residual) 1.264 (0.0487)

------------------------------------------

N 432

------------------------------------------

Standard errors in parentheses

Unfortunately, it is not possible for transform() to turn such correlations into covariances (requires multiplication by the standard deviations). However, you can use estadd to manually compute the terms in advance and add them in the footer of the table. Example:

. xtmixed, variance

Mixed-effects REML regression Number of obs = 432

Group variable: id Number of groups = 48

Obs per group: min = 9

avg = 9.0

max = 9

Wald chi2(1) = 4552.31

Log restricted-likelihood = -870.43562 Prob > chi2 = 0.0000

------------------------------------------------------------------------------

weight | Coef. Std. Err. z P>|z| [95% Conf. Interval]

-------------+----------------------------------------------------------------

week | 6.209896 .0920382 67.47 0.000 6.029504 6.390287

_cons | 19.35561 .4038677 47.93 0.000 18.56405 20.14718

------------------------------------------------------------------------------

------------------------------------------------------------------------------

Random-effects Parameters | Estimate Std. Err. [95% Conf. Interval]

-----------------------------+------------------------------------------------

id: Unstructured |

var(week) | .3799957 .0839023 .2465103 .5857635

var(_cons) | 6.986465 1.616357 4.439432 10.99481

cov(week,_cons) | -.1033632 .2627309 -.6183063 .41158

-----------------------------+------------------------------------------------

var(Residual) | 1.596829 .1231981 1.372736 1.857506

------------------------------------------------------------------------------

LR test vs. linear regression: chi2(3) = 766.07 Prob > chi2 = 0.0000

Note: LR test is conservative and provided only for reference.

. mat list e(b)

e(b)[1,6]

weight: weight: lns1_1_1: lns1_1_2: atr1_1_1_2:

week _cons _cons _cons _cons

y1 6.2098958 19.355613 -.48379761 .97198734 -.06352304

lnsig_e:

_cons

y1 .23401004

. estadd scalar v1 = exp(2*[lns1_1_1]_b[_cons])

added scalar:

e(v1) = .37999574

. estadd scalar v2 = exp(2*[lns1_1_2]_b[_cons])

added scalar:

e(v2) = 6.9864649

. estadd scalar cov = tanh([atr1_1_1_2]_b[_cons]) ///

> * exp([lns1_1_1]_b[_cons]) ///

> * exp([lns1_1_2]_b[_cons])

added scalar:

e(cov) = -.10336316

. estadd scalar v_e = exp(2*[lnsig_e]_b[_cons])

added scalar:

e(v_e) = 1.5968295

. esttab, se wide nostar keep(weight:) obslast ///

> scalars("v1 var(week)" "v2 var(_cons)" ///

> "cov cov(week,_cons)" "v_e var(Residual)") ///

> eqlabels(none) varwidth(15)

-----------------------------------------

(1)

weight

-----------------------------------------

week 6.210 (0.0920)

_cons 19.36 (0.404)

-----------------------------------------

var(week) 0.380

var(_cons) 6.986

cov(week,_cons) -0.103

var(Residual) 1.597

N 432

-----------------------------------------

Standard errors in parentheses

LaTeX

Advanced LaTeX example: Arrange models in groups

. sysuse auto

(1978 Automobile Data)

. eststo: quietly reg weight mpg

(est1 stored)

. eststo: quietly reg weight mpg foreign

(est2 stored)

. eststo: quietly reg price weight mpg

(est3 stored)

. eststo: quietly reg price weight mpg foreign

(est4 stored)

. esttab using example.tex, booktabs label ///

> mgroups(A B, pattern(1 0 1 0) ///

> prefix(\multicolumn{@span}{c}{) suffix(}) ///

> span erepeat(\cmidrule(lr){@span})) ///

> alignment(D{.}{.}{-1}) page(dcolumn) nonumber

(output written to example.tex)

. eststo clear

Result:

Descriptive tables

Table of descriptives

[estpost supersedes this example. See "Post summary statistics (summarize)" or "Post summary statistics (tabstat)" under "Examples for estpost".]

Research papers usually contain a table displaying the descriptive statistics for all variables in the analysis. The following example illustrates how such a table can be produced using estadd summ and esttab. Assume, your analysis uses price as the dependent variable and weight, mpg, and foreign as independent variables. To create a descriptives table including all four variables, type:

. sysuse auto

(1978 Automobile Data)

. generate y = uniform()

. quietly regress y price weight mpg foreign, noconstant

. estadd summ

added matrices:

e(sd) : 1 x 4

e(max) : 1 x 4

e(min) : 1 x 4

e(mean) : 1 x 4

. esttab, cells("mean sd min max") nogap nomtitle nonumber

----------------------------------------------------------------

mean sd min max

----------------------------------------------------------------

price 6165.257 2949.496 3291 15906

weight 3019.459 777.1936 1760 4840

mpg 21.2973 5.785503 12 41

foreign .2972973 .4601885 0 1

----------------------------------------------------------------

N 74

----------------------------------------------------------------

The trick is to generate a fake variable and regress it on all involved variables, including the dependent variable.

Table of descriptives by subgroups

[estpost supersedes this example. See "Post summary statistics by subgroups (summarize)" or "Post summary statistics by subgroups (tabstat)" under "Examples for estpost".]

A table of descriptive statistics by subgroups can easily be produced using by and eststo:

. sysuse auto

(1978 Automobile Data)

. generate y = uniform()

. by foreign: eststo: quietly regress y price weight mpg, nocons

-------------------------------------------------------------------------------

-> Domestic

(est1 stored)

-------------------------------------------------------------------------------

-> Foreign

(est2 stored)

. estadd summ : *

. esttab, main(mean) aux(sd) label nodepvar nostar nonote

----------------------------------------------

(1) (2)

Domestic Foreign

----------------------------------------------

Price 6072.4 6384.7

(3097.1) (2621.9)

Weight (lbs.) 3317.1 2315.9

(695.4) (433.0)

Mileage (mpg) 19.83 24.77

(4.743) (6.611)

----------------------------------------------

Observations 52 22

----------------------------------------------

. eststo clear

Tabulating results from t-Tests

[estpost supersedes this example. See "Post results from two-sample mean-comparison tests (ttest)" under "Examples for estpost".]

Basically anything can be tabulated by estout or esttab once it is posted in e(). Here is an example with t-tests:

. capt prog drop myttests

. *! version 1.0.0 14aug2007 Ben Jann

. program myttests, eclass

1. version 8

2. syntax varlist [if] [in], by(varname) [ * ]

3. marksample touse

4. markout `touse' `by'

5. tempname mu_1 mu_2 d d_se d_t d_p

6. foreach var of local varlist {

7. qui ttest `var' if `touse', by(`by') `options'

8. mat `mu_1' = nullmat(`mu_1'), r(mu_1)

9. mat `mu_2' = nullmat(`mu_2'), r(mu_2)

10. mat `d' = nullmat(`d' ), r(mu_1)-r(mu_2)

11. mat `d_se' = nullmat(`d_se'), r(se)

12. mat `d_t' = nullmat(`d_t' ), r(t)

13. mat `d_p' = nullmat(`d_p' ), r(p)

14. }

15. foreach mat in mu_1 mu_2 d d_se d_t d_p {

16. mat coln ``mat'' = `varlist'

17. }

18. tempname b V

19. mat `b' = `mu_1'*0

20. mat `V' = `b''*`b'

21. eret post `b' `V'

22. eret local cmd "myttests"

23. foreach mat in mu_1 mu_2 d d_se d_t d_p {

24. eret mat `mat' = ``mat''

25. }

26. end

. sysuse auto

(1978 Automobile Data)

. myttests price weight mpg, by(foreign)

. ereturn list

macros:

e(cmd) : "myttests"

e(properties) : "b V"

matrices:

e(b) : 1 x 3

e(V) : 3 x 3

e(d_p) : 1 x 3

e(d_t) : 1 x 3

e(d_se) : 1 x 3

e(d) : 1 x 3

e(mu_2) : 1 x 3

e(mu_1) : 1 x 3

. esttab, nomtitle nonumbers noobs ///

> cells("mu_1(fmt(a3)) mu_2 d(star pvalue(d_p))" ". . d_se(par)")

------------------------------------------------------

mu_1 mu_2 d/d_se

------------------------------------------------------

price 6072.4 6384.7 -312.3

(754.4)

weight 3317.1 2315.9 1001.2***

(160.3)

mpg 19.83 24.77 -4.946***

(1.362)

------------------------------------------------------

(An alternative approach would be to save three sets of estimates, one for each group, and one for the differences.)

Frequency tables

[estpost supersedes this example. See "Post a one-way frequency table (tabulate)" and "Post a two-way frequency table (tabulate)" under "Examples for estpost".]

With a little programming you could even do frequency tables in estout. Here is an example for a one-way table:

. capt prog drop e_tabulate

. *! version 1.0.0 24sep2007 Ben Jann

. prog e_tabulate, eclass

1. version 8.2

2. syntax varname(numeric) [if] [in] [fw aw iw] [, noTOTal * ]

3. tempname count percent vals V

4. tab `varlist' `if' `in' [`weight'`exp'], matcell(`count') matrow(`vals

> ') `options'

5. local N = r(N)

6. mat `count' = `count''

7. forv r =1/`=rowsof(`vals')' {

8. local value: di `vals'[`r',1]

9. local label: label (`varlist') `value'

10. local values "`values' `value'"

11. local labels `"`labels' `value' `"`label'"'"'

12. }

13. if "`total'"=="" {

14. mat `count' = `count', `N'

15. local values "`values' total"

16. local labels `"`labels' total `"Total"'"'

17. }

18. mat colname `count' = `values'

19. mat `percent' = `count'/`N'*100

20. mat `V' = `count''*`count'*0

21. eret post `count' `V', depname(`varlist') obs(`N')

22. eret local cmd "e_tabulate"

23. eret local depvar "`varlist'"

24. eret local labels `"`labels'"'

25. eret mat percent = `percent'

26. end

. sysuse auto

(1978 Automobile Data)

. e_tabulate foreign

Car type | Freq. Percent Cum.

------------+-----------------------------------

Domestic | 52 70.27 70.27

Foreign | 22 29.73 100.00

------------+-----------------------------------

Total | 74 100.00

. ereturn list

scalars:

e(N) = 74

macros:

e(labels) : " 0 `"Domestic"' 1 `"Foreign"' total `"Total"'"

e(depvar) : "foreign"

e(cmd) : "e_tabulate"

e(properties) : "b V"

matrices:

e(b) : 1 x 3

e(V) : 3 x 3

e(percent) : 1 x 3

. mat list e(b)

e(b)[1,3]

0 1 total

y1 52 22 74

. mat list e(percent)

e(percent)[1,3]

0 1 total

c1 70.27027 29.72973 100

. esttab, cell("b percent") noobs nonumbers nomtitles ///

> collabels(Freq. Percent, lhs(`:var lab `e(depvar)'')) ///

> varlabels(`e(labels)', blist(total "{hline @width}{break}"))

--------------------------------------

Car type Freq. Percent

--------------------------------------

Domestic 52 70.27027

Foreign 22 29.72973

--------------------------------------

Total 74 100

--------------------------------------

To construct a twoway table, save the conditional distributions in the table columns as separate estimation sets. Example:

. bys foreign: eststo: e_tabulate rep

-------------------------------------------------------------------------------

-> Domestic

Repair |

Record 1978 | Freq. Percent Cum.

------------+-----------------------------------

1 | 2 4.17 4.17

2 | 8 16.67 20.83

3 | 27 56.25 77.08

4 | 9 18.75 95.83

5 | 2 4.17 100.00

------------+-----------------------------------

Total | 48 100.00

(est1 stored)

-------------------------------------------------------------------------------

-> Foreign

Repair |

Record 1978 | Freq. Percent Cum.

------------+-----------------------------------

3 | 3 14.29 14.29

4 | 9 42.86 57.14

5 | 9 42.86 100.00

------------+-----------------------------------

Total | 21 100.00

(est2 stored)

. esttab, main(percent 2) not nostar mtitles noobs nonote ///

> varlab(`e(labels)', blist(total "{hline @width}{break}"))

--------------------------------------

(1) (2)

Domestic Foreign

--------------------------------------

1 4.17

2 16.67

3 56.25 14.29

4 18.75 42.86

5 4.17 42.86

--------------------------------------

Total 100.00 100.00

--------------------------------------

. eststo clear

Other

Tabulating a Stata matrix

A Stata matrix can be tabulated in estout or esttab by typing matrix(matname) instead of providing a list of names of stored estimation sets. Example:

. matrix A = (11,12,13)\(21,22,23)\(31,32,33)\(41,42,43)

. esttab matrix(A)

---------------------------------------------------

A

c1 c2 c3

---------------------------------------------------

r1 11 12 13

r2 21 22 23

r3 31 32 33

r4 41 42 43

---------------------------------------------------

Numeric formats can be set by adding a fmt() suboption in the matrix() argument. Examples:

. esttab matrix(A, fmt(1 2 3))

---------------------------------------------------

A

c1 c2 c3

---------------------------------------------------

r1 11.0 12.00 13.000

r2 21.0 22.00 23.000

r3 31.0 32.00 33.000

r4 41.0 42.00 43.000

---------------------------------------------------

. esttab matrix(A, fmt("1 2 3 4" "4 3 2 1"))

---------------------------------------------------

A

c1 c2 c3

---------------------------------------------------

r1 11.0 12.0000 13.0

r2 21.00 22.000 23.00

r3 31.000 32.00 33.000

r4 41.0000 42.0 43.0000

---------------------------------------------------

Examples for tabulating a matrix that also contains equation names:

. mat rownames A = "eq1:row1" "eq1:row2" "eq2:row1" "eq2:row2"

. esttab matrix(A)

---------------------------------------------------

A

c1 c2 c3

---------------------------------------------------

eq1

row1 11 12 13

row2 21 22 23

---------------------------------------------------

eq2

row1 31 32 33

row2 41 42 43

---------------------------------------------------

. esttab matrix(A), unstack compress

----------------------------------------------------------------------

A

eq1 eq2

c1 c2 c3 c1 c2 c3

----------------------------------------------------------------------

row1 11 12 13 31 32 33

row2 21 22 23 41 42 43

----------------------------------------------------------------------

. set seed 123

. matrix A = matuniform(4,4)

. mat coleq A = eq1 eq1 eq2 eq2

. mat roweq A = eq1 eq1 eq2 eq2

. esttab matrix(A), eqlabels(,merge)

----------------------------------------------------------------

A

eq1:c1 eq1:c2 eq2:c3 eq2:c4

----------------------------------------------------------------

eq1:r1 .912044 .0075452 .2808588 .4602787

eq1:r2 .5601059 .6731906 .6177612 .8656876

eq2:r3 9.57e-06 .4090917 .7234821 .4862948

eq2:r4 .9899684 .3205308 .1244845 .3839803

----------------------------------------------------------------

Flip models and coefficients (place models in rows instead of in columns)

esttab and estout place different models in separate columns. Sometimes it is desirable, however, to arrange a table so that the models are placed in separate rows. Here are two approaches to construct such a table.

Approach 1: esttab and estout return a matrix r(coefs) that contains the tabulated results. You can run esttab or estout and then run it again in matrix mode to transpose and tabulate r(coefs). This approach is simple but the possibilities for formatting the table are somewhat limited. Example:

. sysuse auto

(1978 Automobile Data)

. eststo model1: quietly reg price weight

. eststo model2: quietly reg price weight mpg

. esttab, se nostar

--------------------------------------

(1) (2)

price price

--------------------------------------

weight 2.044 1.747

(0.377) (0.641)

mpg -49.51

(86.16)

_cons -6.707 1946.1

(1174.4) (3597.0)

--------------------------------------

N 74 74

--------------------------------------

Standard errors in parentheses

. mat list r(coefs)

r(coefs)[3,4]

model1: model1: model2: model2:

b se b se

weight 2.0440626 .37683413 1.7465592 .64135379

mpg .z .z -49.512221 86.156039

_cons -6.7073534 1174.4296 1946.0687 3597.0496

. esttab r(coefs, transpose)

---------------------------------------------------

r(coefs)

weight mpg _cons

---------------------------------------------------

model1

b 2.044063 -6.707353

se .3768341 1174.43

---------------------------------------------------

model2

b 1.746559 -49.51222 1946.069

se .6413538 86.15604 3597.05

---------------------------------------------------

. eststo clear

Approach 2: Again run esttab or estout to compile r(coefs) but then, for each coefficient, collect the results and post them in e() (i.e. post one "model" per coefficient). This approach requires some programming but gives you full flexibility. Example:

. sysuse auto

(1978 Automobile Data)

. eststo model1: quietly reg price weight

. eststo model2: quietly reg price weight mpg

. esttab, se nostar

--------------------------------------

(1) (2)

price price

--------------------------------------

weight 2.044 1.747

(0.377) (0.641)

mpg -49.51

(86.16)

_cons -6.707 1946.1

(1174.4) (3597.0)

--------------------------------------

N 74 74

--------------------------------------

Standard errors in parentheses

. matrix C = r(coefs)

. eststo clear

. local rnames : rownames C

. local models : coleq C

. local models : list uniq models

. local i 0

. foreach name of local rnames {

2. local ++i

3. local j 0

4. capture matrix drop b

5. capture matrix drop se

6. foreach model of local models {

7. local ++j

8. matrix tmp = C[`i', 2*`j'-1]

9. if tmp[1,1]<. {

10. matrix colnames tmp = `model'

11. matrix b = nullmat(b), tmp

12. matrix tmp[1,1] = C[`i', 2*`j']

13. matrix se = nullmat(se), tmp

14. }

15. }

16. ereturn post b

17. quietly estadd matrix se

18. eststo `name'

19. }

. esttab, se mtitle noobs

------------------------------------------------------------

(1) (2) (3)

weight mpg _cons

------------------------------------------------------------

model1 2.044*** -6.707

(0.377) (1174.4)

model2 1.747** -49.51 1946.1

(0.641) (86.16) (3597.0)

------------------------------------------------------------

Standard errors in parentheses

* p<0.05, ** p<0.01, *** p<0.001

. eststo clear

Tabulating results from an r-class program

Many Stata commands and user programs return results in r(). To tabulate such results in estout or esttab you can collect them in a matrix and tabulate the matrix (Approach 1) or post the results as one or more vectors in e() and tabulate them from there (Approach 2). Approach 2 is more flexible than Approach 1.

Approach 1: collect results in a matrix and tabulate the matrix

In the following example

the ineqrbd command by Carlo V. Fiorio and Stephen P. Jenkins is used (see

http://ideas.repec.org/c/boc/bocode/s456960.html).

ineqrbd happens to return results in a series of r()-macros.

We can construct a matrix from these macros (and also compute some additional

results using the formulas provided in ineqrbd's output) and then tabulate

the matrix as follows:

. capture which ineqrbd // check whether -ineqrbd- is installed

. if _rc ssc install ineqrbd // and get it if not

. sysuse auto

(1978 Automobile Data)

. ineqrbd price trunk weight length foreign, noregression

Regression-based decomposition of inequality in price

---------------------------------------------------------------------------

Decomp. | 100*s_f S_f 100*m_f/m CV_f CV_f/CV(total)

---------+-----------------------------------------------------------------

residual | 45.1031 0.2158 0.0000 1.79e+15 3.74e+15

trunk | -0.4687 -0.0022 -2.2943 -0.3109 -0.6499

weight | 81.8711 0.3917 282.5215 0.2574 0.5380

length | -29.2268 -0.1398 -273.2854 -0.1185 -0.2477

foreign | 2.7213 0.0130 17.2635 1.5479 3.2356

---------+-----------------------------------------------------------------

Total | 100.0000 0.4784 100.0000 0.4784 1.0000

---------------------------------------------------------------------------

Note: proportionate contribution of composite var f to inequality of Total,

s_f = rho_f*sd(f)/sd(Total). S_f = s_f*CV(Total).

m_f = mean(f). sd(f) = std.dev. of f. CV_f = sd(f)/m_f.

Total = price

. return list

macros:

r(sf_Z4) : ".0272132003266729"

r(cv_Z4) : "1.547906632830336"

r(sd_Z4) : "1647.497942176796"

r(mean_Z4) : "1064.339351763328"

r(sf_Z3) : "-.2922677469661964"

r(cv_Z3) : "-.1184805603472782"

r(sd_Z3) : "1996.248597028214"

r(mean_Z3) : "-16848.7437194508"

r(sf_Z2) : ".8187108270390759"

r(cv_Z2) : ".2573949336205025"

r(sd_Z2) : "4483.350954895487"

r(mean_Z2) : "17418.17871794494"

r(sf_Z1) : "-.004687100101882"

r(cv_Z1) : "-.3109311493112151"

r(sd_Z1) : "43.98088549818675"

r(mean_Z1) : "-141.4489529132564"

r(sf_Z0) : ".4510308197023296"

r(cv_Z0) : "1790770538833059"

r(sd_Z0) : "1980.84687222313"

r(mean_Z0) : "1.10614220486e-12"

r(cv_tot) : ".4784060098610568"

r(sd_tot) : "2949.49588476892"

r(mean_tot) : "6165.256756756757"

r(total) : " price"

r(xvars) : "trunk weight length foreign"

r(yvar) : "price"

r(varlist) : "price trunk weight length foreign"

. // Step 1: collect results from r(sf_Z#), r(mean_Z#), and r(cv_Z#)

. local xvars "`r(xvars)'"

. local nx : list sizeof xvars

. foreach s in sf mean cv {

2. tempname `s'

3. matrix ``s'' = J(`nx'+2, 1, .z)

4. matrix rownames ``s'' = residual `r(xvars)' Total

5. forv i = 0/`nx' {

6. matrix ``s''[`i'+1, 1] = `r(`s'_Z`i')'

7. }

8. }

. matrix `sf'[rowsof(`sf'), 1] = 1

. matrix `mean'[rowsof(`mean'), 1] = `r(mean_tot)'

. matrix `cv'[rowsof(`sf'), 1] = `r(cv_tot)'

. // Step 2: build matrix that mirrors -ineqrbd-'s output

. matrix ineqrbd = ///

> `sf' * 100 , /// column 1: 100*s_f

> `sf' * `r(cv_tot)' , /// column 2: S_f

> `mean' / `r(mean_tot)' * 100, /// column 3: 100*m_f/m

> `cv', /// column 4: CV_f

> `cv' / `r(cv_tot)' // column 5: CV_f/CV(total)

. matrix colnames ineqrbd = 100*s_f S_f 100*m_f/m CV_f CV_f/CV(total)

. // Step 3: tabulate the matrix

. esttab matrix(ineqrbd)

-----------------------------------------------------------------------------

ineqrbd

100*s_f S_f 100*m_f/m CV_f CV_f/CV(to~)

-----------------------------------------------------------------------------

residual 45.10308 .2157759 1.79e-14 1.79e+15 3.74e+15

trunk -.46871 -.0022423 -2.294291 -.3109311 -.6499315

weight 81.87108 .3916762 282.5215 .2573949 .5380261

length -29.22677 -.1398226 -273.2854 -.1184806 -.2476569

foreign 2.72132 .013019 17.2635 1.547907 3.23555

Total 100 .478406 100 .478406 1

-----------------------------------------------------------------------------

Approach 2: post results as vectors in e()

Instead of directly

tabulating the matrix you can post the matrix columns as vectors in e() and

then tabulate these vectors. This gives you some additional flexibility for formatting

the columns. Here is an example (Stata 9 is required):

. capture which ineqrbd // check whether -ineqrbd- is installed

. if _rc ssc install ineqrbd // and get it if not

. sysuse auto

(1978 Automobile Data)

. ineqrbd price trunk weight length foreign, noregression

Regression-based decomposition of inequality in price

---------------------------------------------------------------------------

Decomp. | 100*s_f S_f 100*m_f/m CV_f CV_f/CV(total)

---------+-----------------------------------------------------------------

residual | 45.1031 0.2158 0.0000 1.79e+15 3.74e+15

trunk | -0.4687 -0.0022 -2.2943 -0.3109 -0.6499

weight | 81.8711 0.3917 282.5215 0.2574 0.5380

length | -29.2268 -0.1398 -273.2854 -0.1185 -0.2477

foreign | 2.7213 0.0130 17.2635 1.5479 3.2356

---------+-----------------------------------------------------------------

Total | 100.0000 0.4784 100.0000 0.4784 1.0000

---------------------------------------------------------------------------

Note: proportionate contribution of composite var f to inequality of Total,

s_f = rho_f*sd(f)/sd(Total). S_f = s_f*CV(Total).

m_f = mean(f). sd(f) = std.dev. of f. CV_f = sd(f)/m_f.

Total = price

. // Step 1: collect results from r(sf_Z#), r(mean_Z#), and r(cv_Z#)

. local xvars "`r(xvars)'"

. local nx : list sizeof xvars

. foreach s in sf mean cv {

2. tempname `s'

3. matrix ``s'' = J(`nx'+2, 1, .z)

4. matrix rownames ``s'' = residual `r(xvars)' Total

5. forv i = 0/`nx' {

6. matrix ``s''[`i'+1, 1] = `r(`s'_Z`i')'

7. }

8. }

. matrix `sf'[rowsof(`sf'), 1] = 1

. matrix `mean'[rowsof(`mean'), 1] = `r(mean_tot)'

. matrix `cv'[rowsof(`sf'), 1] = `r(cv_tot)'

. // Step 2: build matrix that mirrors -ineqrbd-'s output

. matrix ineqrbd = ///

> `sf' * 100 , /// column 1: 100*s_f

> `sf' * `r(cv_tot)' , /// column 2: S_f

> `mean' / `r(mean_tot)' * 100, /// column 3: 100*m_f/m

> `cv', /// column 4: CV_f

> `cv' / `r(cv_tot)' // column 5: CV_f/CV(total)

. matrix colnames ineqrbd = 100*s_f S_f 100*m_f/m CV_f CV_f/CV(total)

. // Step 3: post matrix columns in e()

. ereturn post

. tempname tmp

. local i 0

. foreach col in s_f100 S_f m_f100 CV_f CV_ftot {

2. local ++i

3. matrix `tmp' = ineqrbd[1...,`i']'

4. quietly estadd matrix `col' = `tmp'

5. }

. ereturn list

matrices:

e(CV_ftot) : 1 x 6

e(CV_f) : 1 x 6

e(m_f100) : 1 x 6

e(S_f) : 1 x 6

e(s_f100) : 1 x 6

. // Step 4: tabulate

. esttab, cell("s_f100 S_f m_f100 CV_f CV_ftot") noobs

-----------------------------------------------------------------------------

(1)

s_f100 S_f m_f100 CV_f CV_ftot

-----------------------------------------------------------------------------

residual 45.10308 .2157759 1.79e-14 1.79e+15 3.74e+15

trunk -.46871 -.0022423 -2.294291 -.3109311 -.6499315

weight 81.87108 .3916762 282.5215 .2573949 .5380261

length -29.22677 -.1398226 -273.2854 -.1184806 -.2476569

foreign 2.72132 .013019 17.2635 1.547907 3.23555

Total 100 .478406 100 .478406 1

-----------------------------------------------------------------------------

. esttab, cell((S_f s_f100(fmt(1) par("" "%")))) noobs

--------------------------------------

(1)

S_f s_f100

--------------------------------------

residual .2157759 45.1%

trunk -.0022423 -0.5%

weight .3916762 81.9%

length -.1398226 -29.2%

foreign .013019 2.7%

Total .478406 100.0%

--------------------------------------

Including a column containing bivariate effects (stack models)

estout cannot stack models. A solution is to stack the models in advance and save the result in e(). Here is an example where the goal is to include a column containing the bivariate effects of the regressors:

. capt prog drop appendmodels

. *! version 1.0.0 14aug2007 Ben Jann

. program appendmodels, eclass

1. // using first equation of model

. version 8

2. syntax namelist

3. tempname b V tmp

4. foreach name of local namelist {